2014 Aerospace Fastener Outlook Hits Double Digits

FEATURE

Boeing Moving Fastener Work In-House

Boeing is still trying to bring more fastener work in-house.

One of the drivers behind BA’s new ‘Partnering For Success Program’ is bringing fastener production & procurement in-house.

“BA is currently working with New Breed Logistics to better maintain control of its internal fastener supply – which includes the increased internal fabrication, better inventory management, and concerted effort to reduce the number of SKUs.”

The BA strategy has not impact the distribution channel or supplier base.

“There are multiple contacts who do not believe BA is likely to be successful in controlling the fastener volume due to past failures at other companies who have attempted similar strategies like Spirit Aerosystems (SPR).”

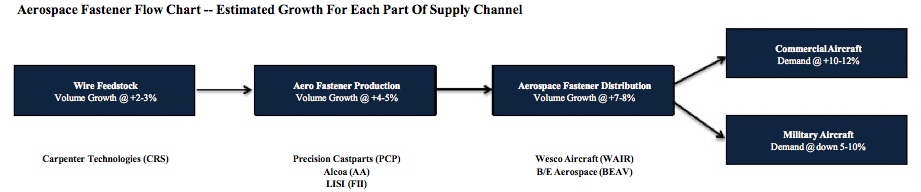

The aerospace fasteners market has seen some moderation in order trends over the past 90 days (at +7-8% growth versus 9%-10% last quarter), according to the AEROSPACE SUPPLY CHAIN REVIEW published by the Cleveland Research Company.

However, the 2014 outlook is holding at 10%-15%, suggesting the airframe market is becoming a stronger pull for the forging segments, which could drive 20%-25% growth over the next 12 months.

“We did not pick up any major changes to the end-market landscape. In general, the aerospace drivers seem to be holding at muted levels (+1-2%), led by slightly better momentum for the downstream fasteners market.”

Channel discussions show continued underlying demand strength for aerospace fasteners, but the data points appear to be modestly lower versus 3Q. Underlying demand growth appears to be slightly weaker versus 3Q, suggesting “slightly more cautious activity at the distribution level and an inventory overhang throughout the rest of the supply base.”

The volume weakness appears to be a temporary factor as the bullish 2014 outlook seems to be holding.

“The channel commentary suggests next year should become a period of accelerated demand growth & backlog expansion… driven by higher commercial aircraft delivery schedules,” the Cleveland Research Company found.

At this point, we believe the distributors are slightly better-positioned in 4Q based on the location of excess inventories in the channel.

Fastener producers are seeing some inventory-related headwinds.

“There appears to be some excess inventory within the channel and certain distributions are staying cautious on the number of held units until order rates accelerate.

“We believe this translates into a 2 point reduction in fabrication comps, estimated at 4%-5% versus 5%-6% last quarter.”

But expectations for 2014 are holding in the 10%-15% range. Major demand drivers will be the increased 787 & 737 delivery schedules, early pull from the A350 program, and the regional jet market.

“This is expected to offset the weakness in military aircraft, which is looking down another 5% for 2014.”

Lead times have moved out by 2-3 weeks since August but pricing power has not increased.

“We calculate the average lead time at 30-32 weeks, which compares to 25-30 weeks at summer end.”

The backlogs have improved considerably from the 14-16 weeks level in mid-2012.

“However, we are not seeing much pricing leverage leading into 2014. Prices are looking flat-to-up-slightly until the lead times reach 40-50 weeks.”

Related Stories:

• Alcoa Inks Long-Term Airbus Deal For Aerospace Parts

Related Links:

{kind=link}

There are no comments at the moment, do you want to add one?

Write a comment